Crop losses can wipe out an entire season’s income. A well-structured agricultural insurance policy protects farmers against such shocks. This guide explains Comprehensive Crop Insurance in India—what it covers, how it works today and how the original Comprehensive Crop Insurance Scheme (CCIS) introduced in 1985 laid the foundation for present-day programs. If you’re comparing benefits, exclusions, premiums, or claim triggers, you’ll find clear, India-specific answers here.Crop insurance is one of the most effective tools to safeguard farmers.

- Buy in easy steps

- Premium Starts at INR 499

- Protect 100+ Crops

- Quick & Easy Claims

Direct answer: The Comprehensive Crop Insurance Scheme (CCIS) was introduced in 1985 by the Government of India., Today, farmers typically get comprehensive crop insurance via PMFBY (Pradhan Mantri Fasal Bima Yojana) and Weather-Based Crop Insurance—covering major natural risks, pests, and diseases using area/yield or weather triggers.

Key benefit: Stabilizes farm income after yield loss; premiums are subsidized for notified crops under PMFBY., How claims work: Payouts are triggered by shortfall in area yield (vs. threshold yield) or adverse weather indices—no individual loss survey needed for yield-based schemes.

Who should opt: Borrower and non-borrower farmers growing notified crops, especially in risk-prone districts., What to check before buying: Notified crops/area, sum insured, basis of loss assessment (yield vs. weather), exclusions, timelines for enrollment and claims.

What Is Comprehensive Crop Insurance?

Comprehensive Crop Insurance is an agricultural insurance policy that protects farmers against major production risks—drought, flood, cyclone, unseasonal rain, pest attacks, and plant diseases—so that a bad season does not become a financial crisis. In India, this protection is primarily delivered via government-backed schemes like PMFBY (yield-based) and Weather-Based Crop Insurance (index-based). Private insurers administer these with state and central support.

Why It Matters for Indian Agriculture

Indian farmers face high high weather variability and rising input costs. Comprehensive protection helps stabilize net income, improves credit access, and supports resilience across Kharif and Rabi seasons. For tenant, small and marginal farmers, subsidized premiums make protection accessible.

Quick Background: CCIS 1985 to Today

The original Comprehensive Crop Insurance Scheme (CCIS) was introduced in 1985 as part of government schemes . It was an early, area-yield based program covering selected crops and regions. Over time, India transitioned to broader, more data-driven schemes—NAIS, MNAIS, and now PMFBY—expanding coverage, improving actuarial pricing, and strengthening claim assessment through Crop Cutting Experiments (CCEs), remote sensing, and digital tools.

How Comprehensive Cover Works (Current Models)

1. PMFBY (Yield-Based)

- Coverage: Notified food crops, oilseeds, and commercial/horticulture crops.

- Trigger: Shortfall in area yield vs. threshold yield (based on historical data and CCEs).

- Sum Insured: Typically based on scale of finance or cost of cultivation for the notified crop.

- Premiums: Farmers pay a capped share (e.g., 2% Kharif food crops, 1.5% Rabi food crops, 5% commercial/horticulture); balance subsidized by governments.

- Who should choose: Farmers who want protection against yield loss from multiple perils and prefer objective, area-based assessment.

2. Weather-Based Crop Insurance (Index-Based)

- Coverage: Weather perils (deficit/excess rainfall, heat/cold waves, humidity, wind speed) as per index.

- Trigger: Deviation in weather parameters at reference stations as per policy index.

- Payout speed: Often faster due to parametric structure.

- Who should choose: Farmers exposed to critical weather risks seeking quicker, data-driven payouts.

Advantages of Crop Insurance (Farmer-Centric Benefits)

- Income Stability: Offsets yield losses, protecting working capital and family expenses.

- Credit Support: Eases access to crop loans and prevents debt traps after bad seasons.

- Risk Sharing: Transfers catastrophic risk away from the farmer to the insurer and the scheme.

- Subsidized Premiums: Government support makes protection affordable for small and marginal farmers.

- Confidence to Invest: Encourages adoption of high-yield seeds, balanced fertilization, and mechanization.

What Is Covered vs. Not Covered

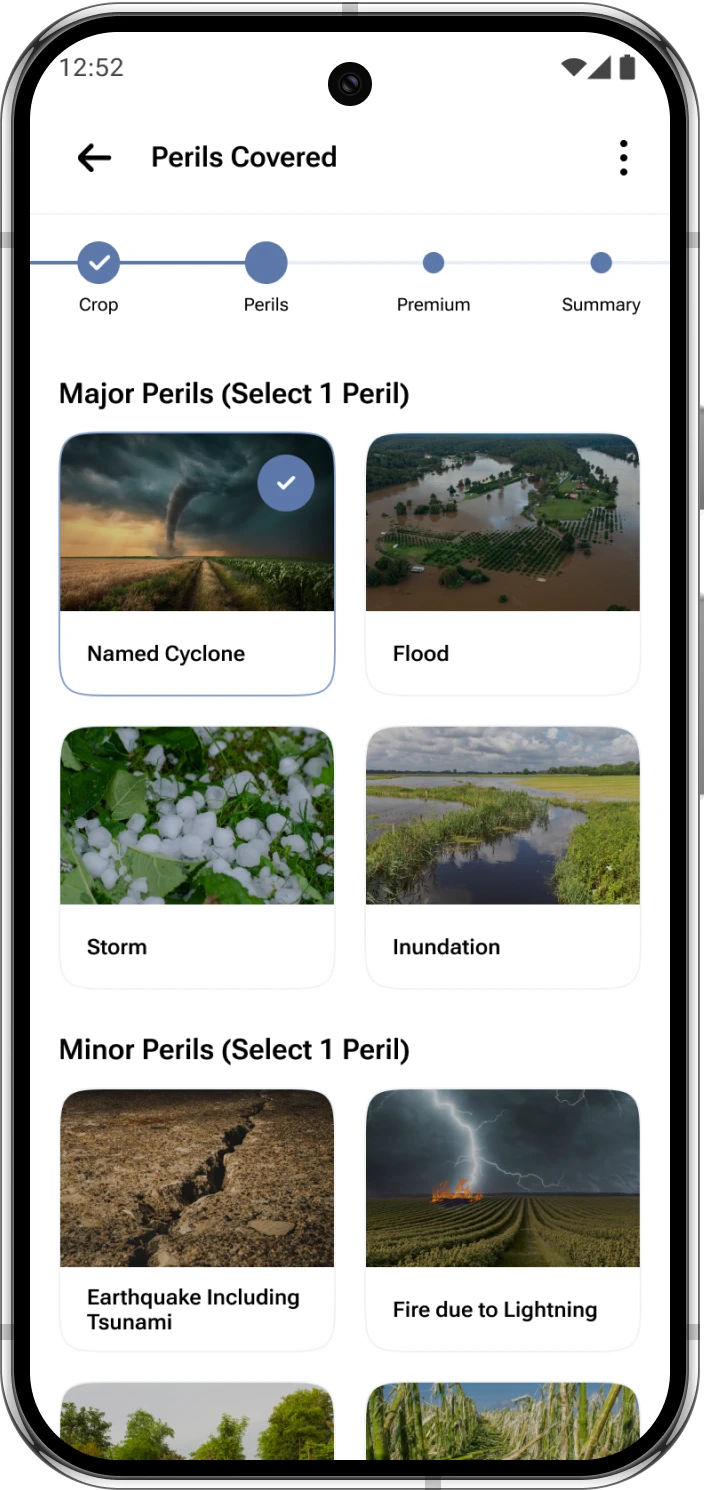

Typically Covered Perils

- Widespread drought or dry spells

- Flood, inundation, and cyclone

- Unseasonal or excessive rainfall and hailstorms (as per scheme terms)

- Pest and disease outbreaks causing yield loss

Common Exclusions

- Preventable losses due to negligence or avoidable agronomic practices

- Losses from war, nuclear risks, or malicious damage

- Post-harvest losses beyond the permitted window or outside notified causes

- Losses from non-notified crops/areas or outside policy period

Eligibility, Enrollment, and Timelines

- Who can enroll: Borrower (loanee) and non-borrower farmers cultivating notified crops/areas.

- Documents: Land records/tenancy proof, sowing certificate (as applicable), bank details, Aadhaar, and crop declaration.

- When to enroll: Before season cut-off dates notified by the state (separate for Kharif/Rabi and for each scheme).

- How to enroll: Via bank/CSC/insurer portal/state portal; confirm your notified crops and sum insured.

Understanding Sum Insured and Premium

Sum Insured (SI): Usually linked to scale of finance or cost of cultivation per hectare for the notified crop. Choose accurate area and crop to avoid underinsurance.

Premium: Farmer share is capped for PMFBY; governments subsidize the rest. For weather-based products, rates depend on the local risk profile and index design.

How Claims Are Assessed and Paid

Yield-Based (PMFBY)

- Assessment: Area-wise CCEs determine actual yield. If it falls below threshold yield, payouts are calculated proportionally for all insured farmers in that unit.

- No individual survey: Claims are area-triggered, reducing delays and disputes.

- Payment: Credited directly to the insured farmer’s bank account after declaration.

Weather-Based (Index)

- Assessment: Weather station data vs. predefined triggers.

- Speed: Often quicker as it avoids field yield measurement.

Real-World Scenarios

- Drought in Kharif: Below-normal rainfall reduces paddy yield. PMFBY triggers payout when area yield dips under threshold, covering input costs.

- Excess Rainfall Event: Heavy downpour damages soybean during flowering. Weather index breach leads to a parametric payout.

- Pest Outbreak: Widespread pest attack cuts yields. Under PMFBY, the area’s yield shortfall triggers compensation.

Comparing Key Agricultural Insurance Options

Steps to Choose the Right Policy

- Confirm if your crop and village are notified under PMFBY or WBCIS this season.

- Check basis of loss you prefer: yield-based vs. weather index.

- Review sum insured, premium share, and subsidy.

- Note cut-off dates and required documents.

- Disclose accurate crop area and sowing details to avoid claim issues.

Historical Note: CCIS 1985

Where Kshema Fits In

Comparison of Crop Insurance Schemes

| Feature | CCIS (1985) | PMFBY (Current) | Weather-Based (Current) |

|---|---|---|---|

| Assessment Basis | Area yield (limited crops/areas) | Area yield via CCEs and historical data | Weather index (rainfall, temperature, etc.) |

| Perils | Major natural perils causing yield loss | Wide set of weather, pest, and disease risks | Specified weather deviations as per index |

| Premium Structure | Subsidized, flat-rated (legacy) | Farmer share capped; balance subsidized | Risk-based; may be subsidized if notified |

| Payout Trigger | Shortfall in area yield | Shortfall in area yield vs. threshold | Index breach at reference station |

| Payout Speed | Longer (legacy processes) | Improved with digital CCE/remote sensing | Often faster due to parametric design |

| Who It Suits | Historical foundation scheme | Farmers seeking comprehensive yield cover | Farmers prioritizing quick, weather-triggered payouts |

| Benefits | Exclusions/Limitations |

|---|---|

| Stabilizes farm income after bad seasons | Non-notified crops/areas are not covered |

| Improves access to formal credit | Negligence or avoidable agronomic failures not covered |

| Government subsidies reduce costs | Losses outside policy period or beyond post-harvest window |

| Objective, area-based payouts reduce disputes | Local losses may not trigger payout if area yield/index not breached |

Conclusion

Comprehensive Crop Insurance protects farm income against major production risks. India’s journey from CCIS (1985) to PMFBY and Weather-Based products has made coverage broader, more data-driven, and more accessible. To choose wisely, verify notified crops/areas, understand whether your risk is best covered by yield or weather triggers, and enroll before cut-off dates. For clear terms, digital support, and help with documentation,explore Kshema’s comprehensive insurance solution that prioritize transparency and timely service.

Department of Agriculture & Farmers Welfare – Crop Insurance Division page