Farmers face increasing climate variability, input cost pressures, and market uncertainty. Adopting crop insurance is one of the most practical strategies to protect farm incomes and enable investment in productivity. This article explains the benefits of crop insurance for farmers, how modern agricultural insurance in India (and beyond) works, and practical steps farmers and agribusinesses can take to get covered quickly and affordably.

Read on for a guide that helps farmers, advisors, and policy makers understand the immediate value and long-term advantages of crop insurance.

- Buy in easy steps

- Premium Starts at INR 499

- Protect 100+ Crops

- Quick & Easy Claims

Crop insurance reduces income volatility, speeds recovery after crop loss, and unlocks credit & investment opportunities for farmers.

Key benefits of crop insurance for farmers at a glance:

- Income protection against weather, pests and other perils,

- Faster claims and payouts with digital-first insurers,

- Improved access to credit and inputs (seed, fertilizer, machinery),

- Incentives from government agri insurance schemes and subsidies,

- Encourages adoption of better farming practices and risk management

Who should read this: smallholders, commercial farmers, lenders, and agri-policy makers looking for practical steps to adopt crop insurance in 2025 and beyond.

| Feature | Yield-based (Indemnity) | Area-yield | Weather-index | Revenue |

|---|---|---|---|---|

| Payout basis | Farm-level measured yield shortfall | Average yield shortfall in an area | Weather trigger (e.g., rainfall, temperature) | Yield and market price combined |

| Speed of payout | Slower (surveys) | Faster | Fastest (automated triggers) | Varies |

| Cost | Higher | Lower | Low–Medium | Medium–High |

| Best for | High-value, small plots needing precision | Smallholders in homogeneous regions | Regions with reliable weather data | Farmers exposed to price risk |

Additionally, short checklist for farmers before buying insurance:

- Verify land records and crop plan

- Check net premium after subsidy

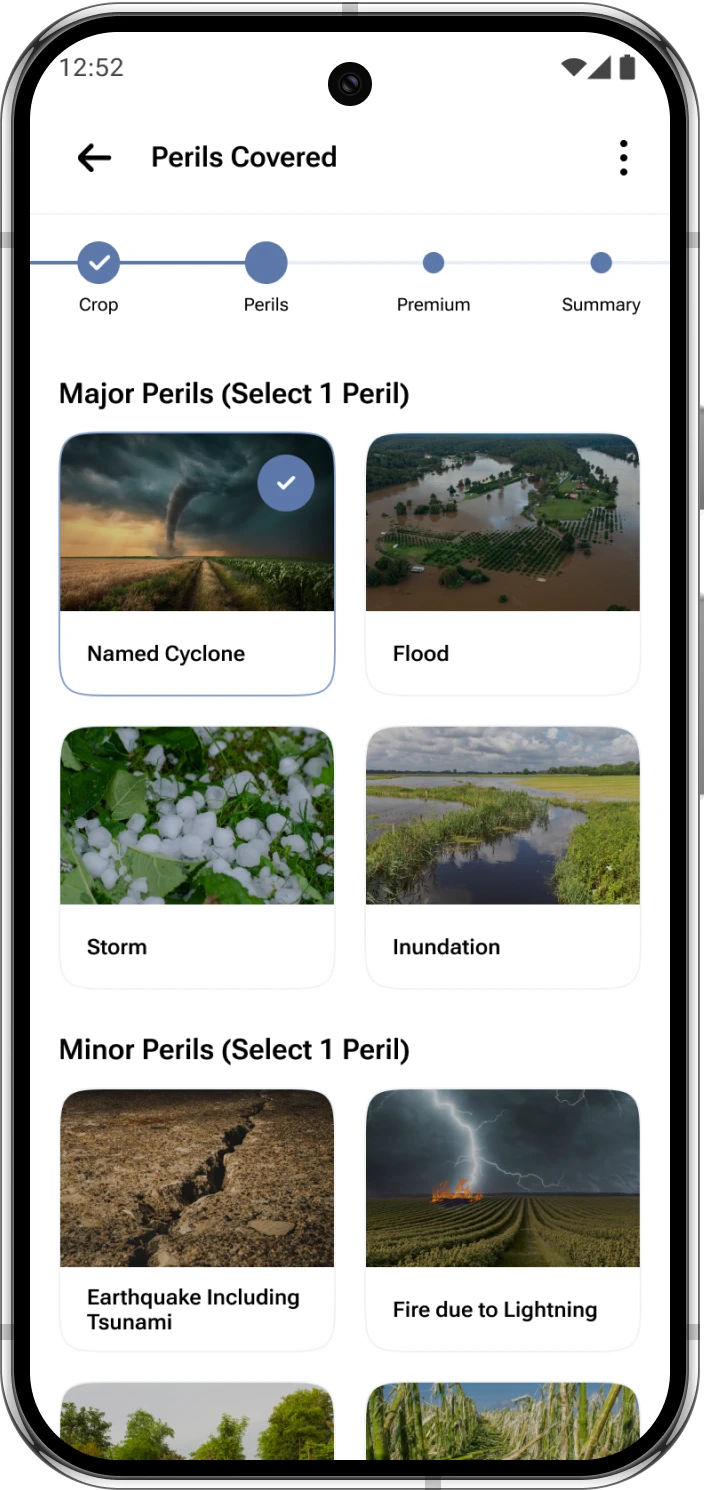

- Confirm covered perils and waiting period

- Ask about claim settlement time and grievance process

- Keep photo documentation and input receipts

The Challenges Faced by Small and Marginal Farmers

- Unpredictable Weather: With climate change, events such as cyclones, floods, hailstorms, unseasonal rainfall etc. have become more frequent and severe.

- Pests and Diseases: Crops are susceptible to pest infestations and diseases, which can destroy entire crops.

- Rising Input Costs: Seeds, fertilisers, and pesticides have become costlier, increasing production expenses for farmers.

- Market Instability: Farmers are often forced to sell their produce at lower prices due to market fluctuations and lack of bargaining power.

- Debt Traps: Without adequate financial security, farmers are compelled to take loans, often at high interest rates, leading to debt cycles.

Why crop insurance matters today

Climate change, rising input costs, and supply-chain shocks make crop losses more frequent and costly.

Crop insurance transfers production risk from farmers to insurers, stabilizing incomes and enabling more predictable farm planning.

Government‑backed schemes such as the Pradhan Mantri Fasal Bima Yojana (PMFBY) play a crucial role in empowering farmers by protecting them against crop loss and income instability. [pmfby.gov.in]

The primary objectives of crop insurance

- Protect farmer income

- Enable faster recovery after loss

- Promote investment in technology and inputs

- Support rural credit markets

Key benefits of crop insurance for farmers

1. Income stability and financial resilience

Insurance compensates for yield or revenue shortfalls due to drought, flood, pest outbreaks, or other insured perils.This reduces the need to sell assets or cut back on essential farm investments.

2. Faster post-loss recovery with digital claims

Digital-first insurers (including many new players in India) reduce survey and claim timelines, delivering quicker payouts. so farmers can buy seeds and inputs for the next sowing season.

3. Better access to credit and input financing

Insured crops are treated as lower-risk collateral by banks and NBFCs, making loans easier and often cheaper to obtain for working capital and capital expenditures.

4. Government scheme integration and subsidies

Many countries, including India, offer premium subsidies through national and state-level schemes such as PMFBY. These programs significantly reduce farmer out-of-pocket premiums and expand overall coverage.

5. Encouragement of good farming practices

Index-based and area-yield insurance schemes often incentivize the use of recommended seeds, optimal planting windows, and standard agronomic practices to reduce loss frequency.

6. Peace of mind and improved decision-making

When downside risk is capped, farmers can plan for the long term—adopting crop rotation, diversification,

and investing confidently in machinery and technology.

Types of crop insurance and how they work

1. Yield-based insurance (indemnity)

Payouts are linked to measured farm-level yield shortfalls compared to a guaranteed or historical yield benchmark.

2. Area-yield insurance

Compensation is triggered when average yields in a defined geographic area fall below a threshold.

These schemes have lower administrative costs and reduced moral hazard.

3. Weather-index insurance

Payouts are automatically triggered by weather events—such as rainfall deficits or heat stress—recorded by trusted sensors,

weather stations, or satellites.

4. Revenue insurance

Revenue insurance covers both yield losses and price fluctuations, offering protection against combined production and market risks.

Choosing the right product

The right insurance product depends on crop type, farm size, data availability, and whether the priority is payout speed, accuracy, or broader area coverage.

How crop insurance fits into India’s agri-insurance landscape (2025 perspective)

Current schemes and trends

- Government programs such as PMFBY continue to shape India’s coverage models.

- Key trends in 2025 include increased private-sector participation, tech-driven claims processing,

and hybrid public–private insurance frameworks.

Role of private digital insurers

Private insurers are improving farmer experience through faster onboarding, smartphone-based surveys,

satellite and AI-led loss assessment, and transparent digital claim tracking.

Regulatory and subsidy considerations

Farmers should evaluate the net premium after subsidies, claim settlement ratios, covered perils,

exclusions, and waiting periods before choosing a policy.

Practical steps for farmers to adopt crop insurance

Step 1 — Assess risk and choose coverage level

Estimate potential yield and revenue exposure, then choose a sum insured that balances adequate protection

with affordable premiums.

Step 2 — Compare products and providers

Compare claim settlement timelines, inclusion of pest or post-harvest risks, and the suitability of

index-based versus indemnity coverage for your land parcel.

Step 3 — Prepare documentation and digital enrolment

Keep land records, crop details, and historical yield data ready.

Many insurers now allow mobile-based enrollment using photos and geo-tagging.

Step 4 — Maintain records and follow recommended practices

Document sowing dates, inputs, and field conditions with photos and logs to speed up claims and minimize disputes.

Step 5 — File claims early and use grievance redressal channels

Adhere strictly to claim timelines and use insurer apps or government grievance portals for faster issue resolution.

Why Crop Insurance in India is Essential for Small and Marginal Farmers

- Protection Against Uncertainties Farmers are at the mercy of nature, more so in a country like India, and adverse weather can wipe out their crops. Crop insurance in India provides financial support during such losses, ensuring that farmers can recover and prepare for the next sowing season.

- Financial Stability A single crop failure can push small and marginal farmers into debt or force them to sell their assets. Crop insurance in india offers protection, enabling them to sustain their livelihoods without resorting to desperate measures.

- Mitigating Debt Dependency Many small farmers rely on informal credit sources that charge exorbitant interest rates. Crop insurance reduces this dependency by creating a financial safety net with the money received as part of the claim settlement process providing aid during distress.

- Long-Term Sustainability Crop insurance also incentivises farmers to adopt and invest in modern, and sustainable farming practices by taking away the fear of financial loss, reducing risks in the long run.

Cost, subsidies, and affordability

Understanding premiums

Premiums depend on crop type, location, sum insured, deductibles, and risk profile.

Area-index products generally cost less than farm-level indemnity insurance.

Government support and subsidy models

Eligible farmers should leverage central and state subsidies, which can dramatically reduce net premium payments,

especially for small and marginal farmers.

Tips to lower net cost

- Choose area-yield insurance where appropriate

- Opt for slightly higher deductibles to reduce premiums

- Bundle insurance with crop loans or input packages

Common concerns and how they’re addresse

Concern — Delayed claims

Digital loss assessment, satellite verification, and pre-defined payout triggers in index-based insurance

have significantly shortened claim settlement timelines.

Concern — Basis risk in index insurance

Hybrid insurance models and denser sensor networks are reducing basis risk.

Farmers seeking higher accuracy can opt for indemnity-based products.

Concern — Policy complexity

Insurers, agri-extension officers, and digital aggregators now provide policy explanations, FAQs,

and helplines in local languages to simplify decision-making.

Who benefits most from crop insurance

Small and marginal farmers gain financial security and improved access to credit,

while medium and large farms benefit from revenue stability that supports long-term investment and productivity growth.

How insurers and stakeholders can improve adoption

Adoption can be accelerated by simplifying products, improving farmer awareness,

expanding mobile-based enrollment, bundling insurance with credit,

and investing in satellite and sensor infrastructure for faster, fairer claims.

Benefits of crop insurance for farmers in India for Small and Marginal Farmers

- Comprehensive Coverage: Crop insurance in India covers losses due to natural calamities, and even wild animal attacks.

- Affordable Premiums: Crop insurance products like Kshema Sukriti make crop insurance affordable even for marginal farmers.

- Protection from Income Shocks: Settlement of insurance claims safeguards the financial interest of the farmers by ensuring they have access to resources to continue farming.

- Empowerment: Crop insurance in India instills confidence in farmers, empowering them to focus on improving productivity rather than worrying about risks.

- Boosts Rural Economy: When farmers are financially secure, they can contribute to the rural economy by investing in inputs, machinery, and labour.

How Crop Insurance Schemes Work in India

- Enrollment: Farmers can enroll in crop insurance schemes in India through banks, insurance companies, Common Service Centers (CSCs) or mobile apps. They must provide details about their land, crops, Aadhaar, etc.

- Premium Payment: Farmers pay a small premium against a sum insured for their insured crop.

- Loss Reporting: In the event of crop loss, farmers report the damage to their insurance provider or local authorities. They can upload photos and/or videos of the crop damage to report loss.

- Claim Settlement: After verification, the insurer processes the claim and disburses the settlement to the farmer.

Role of Kshema General Insurance in Safeguarding the Small and Marginal Farmers

Our Key Offerings Include:

- Comprehensive or customisable protection against losses caused by 8 perils.

- Coverage for damage caused by wild animals like elephants, wild boars, monkeys, and rabbits.

- Simplified enrollment and claims processes using the Kshema app to ensure ease of access for farmers.

Conclusion

Crop insurance is a practical tool that safeguards farmer incomes, speeds recovery after losses, and unlocks credit and investment—making it central to resilient farm livelihoods and modern agricultural growth. For farmers in India and elsewhere, selecting the right product (area-index vs indemnity vs revenue), checking net premium after subsidies, and using digital enrollment and record-keeping will maximize the benefits of crop insurance for farmers.

Ready to protect your harvest? Speak to an insurer or your local agri-extension to compare options and enroll before the next sowing season.

At Kshema General Insurance, we stand by Indian farmers, offering them the tools and support they need to thrive. If you are a farmer looking to secure your crops and livelihood, explore our crop insurance solutions today. Let’s work together to build a resilient farming community for a better tomorrow.

Frequently Asked Questions (FAQs)

1. What are the main benefits of crop insurance for farmers?

The main benefits of crop insurance for farmers include income protection against unpredictable losses (weather, pests), faster recovery through timely claim payouts, improved access to credit, and incentives from government agri insurance schemes. Overall, crop insurance reduces financial volatility and supports investment in farm productivity—summarized as the core benefits of crop insurance for farmers.

2. How does crop insurance in India work in 2025 and what schemes are available?

In India, growers can access a mix of government-backed programs (like PMFBY variants) and private digital insurers. Schemes include area-yield, yield-indemnity and weather-index products. Many 2025 offerings emphasize digital enrollment, satellite-based loss assessments, and hybrid public–private delivery to speed claims and expand coverage.

3. Can crop insurance help small and marginal farmers get loans?

Yes. Insured crops reduce lender risk and can make it easier for small and marginal farmers to obtain working capital and term loans. Banks and NBFCs often accept insured crops as better collateral, and some credit products are bundled with insurance at discounted net premiums.

4. What factors should a farmer consider when choosing a crop insurance policy?

Consider type of coverage (yield, area, weather-index or revenue), net premium after any subsidy, claim settlement history and timelines, listed perils and exclusions, and whether the product suits farm scale and crop type. Also check if the insurer provides digital claim processes and local-language support.

5. Is weather-index insurance reliable despite basis risk?

Weather-index insurance is fast and low-cost, but can have basis risk if station data or satellite measurements don’t reflect a particular plot’s microclimate. Reliability improves with more dense sensor networks, better modeling and hybrid products that combine index triggers with limited farm-level checks.